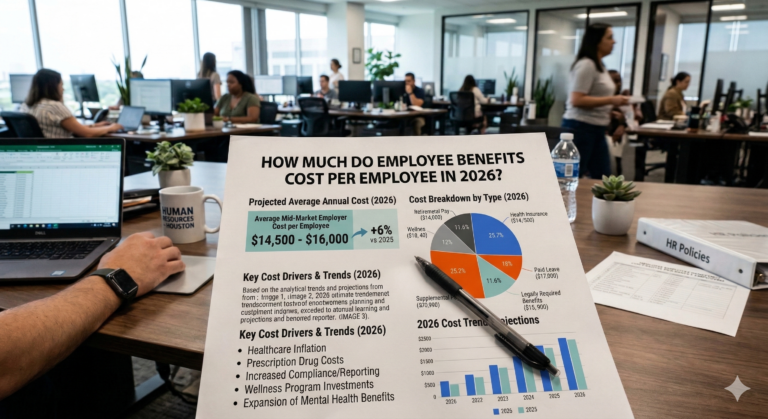

How Much Do Employee Benefits Cost Per Employee in 2026

Key Cost Benchmarks for Mid-Market Employers

- Total benefits cost: 25–40% of base payroll — for a company with 200 employees averaging $75,000 in salary, that’s $3.75M–$6M in annual benefits spend.

- Health insurance alone averages $8,000–$14,000 per employee per year in employer cost, depending on plan design, geography, and workforce demographics.

- Mid-market employers absorbed the 2023–2025 cost increases more often than small businesses — large groups kept deductibles flat while smaller groups raised cost-sharing to offset 6–7% annual premium inflation.

- The employer/employee premium split varies by company size and industry — single coverage is typically 70–85% employer-paid; family coverage ranges from 50–70%.

- 401(k) matching adds 2–5% of payroll to total compensation costs — an often-underestimated variable in total benefits budget planning.

Every time a CFO builds a headcount model, the benefits cost assumption drives the number. Get it wrong and you’re either under-budgeting by six figures or padding the model with phantom costs that kill a hire. The problem is that “average benefits cost per employee” statistics are almost meaningless without the company size, industry, and geographic context that makes them comparable to your specific situation.

This guide breaks it down by company size, benefit category, and the structural decisions — plan design, employer contribution strategy, self-funding vs. fully insured — that actually drive what you spend. These are the numbers that matter for a mid-market employer with 100–500 employees managing a real benefits program.

How Does Your Benefits Spend Compare?

Hotaling’s advisors run independent cost benchmarking for mid-market employers before every renewal — comparing your total benefits spend against industry-specific peer data matched to your company size and geography.

Request a Cost Benchmarking ReviewThe Real Total Benefits Cost Per Employee

The BLS and Kaiser Family Foundation publish aggregate national averages — useful for context, not for budgeting. Here’s what the numbers actually look like for mid-market employers managing a competitive benefits program.

Health insurance (employer cost per employee per year):

- 100-employee company — $9,000–$12,000 for single coverage; $22,000–$28,000 for family coverage. Total employer cost depends heavily on how many employees elect family vs. single coverage.

- 250-employee company — $8,500–$11,500 for single coverage; $20,000–$26,000 for family. Slightly better carrier leverage; more meaningful claims data for underwriting.

- 500-employee company — $8,000–$11,000 for single; $18,000–$24,000 for family. At this size, self-funding or level-funding starts delivering material savings for employers with favorable demographics.

Why these ranges are wide: Health insurance cost per employee is the product of plan design (deductible, network tier, out-of-pocket maximum), workforce demographics (age distribution, dependent enrollment rate, claims history), geography (Texas generally cheaper than California or New York), and employer contribution strategy. A company paying 85% of family premium has dramatically different per-employee cost than one paying 60%, even if they’re on the same carrier plan.

Breaking Down Benefits Cost by Category

Total benefits cost is the sum of multiple lines. CFOs building headcount models need each line separately — the health insurance budget and the retirement budget are managed differently, and collapsing them into a single percentage of payroll obscures where the real variability lives.

Health insurance: The dominant variable. For a mid-market employer on a fully insured plan, expect $600–$1,100 per employee per month in total employer cost (not premium — your contribution). The specific number depends on plan tier, network, and the split you’ve structured. The employer’s contribution to family-tier coverage is where most of the cost concentration lives — most of your higher earners are on family plans.

Dental and vision: Dental typically runs $400–$700 per employee per year in employer cost. Vision is usually $100–$200 per employee per year. Combined, these are relatively small lines — but they show up in benchmarking comparisons and matter to employees more than the cost would suggest.

Life and disability: Group term life at 1–2x annual salary typically costs $150–$400 per employee per year for the employer. Short-term disability runs $200–$500 per employee per year depending on benefit level and elimination period. Long-term disability adds $300–$600 per employee per year. Many mid-market employers offer basic coverage as employer-paid and provide voluntary buy-up options at employee expense.

401(k) matching: A dollar-for-dollar match on the first 4% of salary — a competitive but not maximum formula — costs exactly 4% of compensation for every participating employee who contributes 4% or more. For a 200-person company with average salary of $80,000 and 80% participation, that’s approximately $512,000 per year. The vesting schedule affects when you’re actually paying it vs. when it’s accruing.

FSA/HSA employer contributions: Some mid-market employers make seed contributions to HSA accounts — typically $500–$1,500 per employee per year — as part of a high-deductible plan strategy. This offsets employee out-of-pocket exposure while keeping premium costs lower. The net total benefits cost is often comparable; the employer just shifts the spending from premium to HSA contribution.

Voluntary and supplemental benefits: These are typically employee-paid, but not always. Accident, critical illness, and hospital indemnity products can be offered at zero employer cost as employee-paid options. Some mid-market employers subsidize these to increase enrollment and perceived value.

What Drives Cost Variation — and What You Can Control

Mid-market employers spent significant energy in 2023–2025 trying to hold benefits cost increases below the 6–7% annual premium inflation rate. The employers who did it successfully used specific levers — not carrier switches, which rarely produce sustained savings.

The most effective cost levers for a 100–500 employee employer:

- Plan design adjustment — moving from a $1,500 to $2,000 deductible with an employer-funded HSA contribution of $500 often reduces total employer cost (premium + HSA) by 8–12% while keeping employee out-of-pocket exposure flat. This is the lever most mid-market employers underuse because their broker defaults to keeping the plan design stable at renewal.

- Network tier strategy — adding a tiered network option (narrow network at lower employee contribution, broader network at higher cost) gives cost-conscious employees a choice without cutting coverage for those who need specialist access.

- Self-funding or level-funding — for companies with 150+ employees and stable claims history, moving off a fully insured platform to self-funding or level-funding can produce 5–15% in long-term savings. The trade-off is claims volatility in bad years; stop-loss insurance manages the catastrophic tail.

- Contribution strategy optimization — the employer/employee premium split on family tier is where the most dollars move. A company paying 70% of family premium for a $28,000 plan is paying $19,600 per family-enrolled employee per year. Adjusting to 65% saves $1,400 per family-enrolled employee — meaningful at scale, modest in individual impact.

- Benefit utilization analysis — some benefits in your program are valued highly by employees and well-utilized. Others are expensive and rarely used. An annual utilization analysis identifies where you’re spending money on benefits that don’t improve your competitive position.

The 401(k) Cost Variable Most CFOs Underestimate

Health insurance dominates the benefits cost conversation, but the 401(k) match is the second-largest variable in most mid-market benefits budgets — and it’s increasingly a talent competition factor. Sequoia’s 2025 benchmarking data shows 5% of employers planning to introduce or increase matching contributions, meaning the competitive baseline is moving.

The most common mid-market match formulas and their total cost:

- 50% match on first 6% (the classic “3% effective match”) — costs 3% of compensation for employees contributing 6%+; typically the minimum competitive threshold in most industries

- Dollar-for-dollar on first 4% — costs 4% of compensation; increasingly common among mid-market tech, professional services, and financial services employers competing for knowledge workers

- Dollar-for-dollar on first 6% — costs 6% of compensation; top-quartile match for mid-market employers; competitive with enterprise-level programs in most labor markets

For a 200-person company with $80,000 average salary and 80% 401(k) participation: the 3% effective match costs approximately $384,000 per year. Moving to a 4% effective match adds $128,000 to that number. Moving to a 6% effective match adds $384,000. Whether that investment is justified depends entirely on whether your current match is limiting hiring or contributing to turnover — which is a benchmarking question.

How Company Size Affects Your Carrier Leverage

Everything about health insurance cost negotiation depends on your leverage with carriers — and leverage comes from size, claims history, and the volume of premium your broker places. This is the practical reason why a mid-market company working with a dedicated advisory broker gets meaningfully better rates than the same company working with a generalist.

At 100 employees, you’re in the “small large group” market. Carriers are willing to rate you competitively but have limited actuarial data on your specific claims experience. At 250 employees, you have enough claims history to be rated partially on your own experience rather than purely on manual rates. At 500 employees, you’re a meaningful account and carriers compete aggressively for the renewal.

What this means practically:

- A 100-person employer working through a broker with $300M in managed premium gets rates their 100-person enrollment alone could not access — the carrier is pricing the aggregate relationship, not just your account

- Competitive bidding — getting renewal quotes from multiple carriers — is more important at 100 employees than at 500, because your incumbent has less to lose from losing you and more pricing flexibility to recover at renewal

- The move to self-funding becomes progressively more attractive as you scale; at 500 employees you have enough data to manage the actuarial risk, and the savings from eliminating carrier profit margin and state insurance premium taxes become material

Building Your Benefits Cost Model for Headcount Planning

For CFOs building a headcount model, here’s a practical mid-market benefits cost framework that accounts for the major variables:

- Fully-loaded benefits cost per FTE: Take your annual benefits budget, divide by headcount, and compare to 25–40% of average base salary as a reasonableness check. Under 20% suggests underinsured or bare-bones benefits. Over 45% suggests either an unusually rich program or significant adverse selection in your health claims.

- New hire benefits cost for modeling: Use $12,000–$16,000 per new employee as a placeholder for health, dental, vision, life, and disability — add the 401(k) match separately as a percentage of target salary. Adjust for geography: Houston runs 10–15% below national average; New York City runs 15–20% above.

- Annual cost inflation assumption: Plan for 6–8% medical trend in your benefits budget. If your broker is promising to hold increases to 3%, ask to see the plan design assumptions behind that number — a 3% premium increase usually involves a deductible adjustment or employer contribution change that shifts cost to employees.

Frequently Asked Questions

What percentage of payroll should employee benefits represent? +

The BLS Employment Cost Index consistently shows that benefits represent 25–40% of total compensation for private sector employers. The specific percentage depends heavily on industry (healthcare and finance tend toward the high end; retail and hospitality toward the low end), company size (larger employers generally spend more per employee in absolute terms), and geographic market.

For budgeting purposes, a mid-market employer with a competitive but not lavish program should model 30–35% of base payroll as total benefits cost — health, dental, vision, life, disability, 401(k) match, and statutory payroll taxes combined. If your number is materially below 28%, you’re likely below market on at least one major benefit line.

Is self-funding worth it for a 150-employee company? +

It depends on your workforce demographics and claims history. The primary benefits of self-funding are: you keep the underwriting profit your carrier charges in the fully insured premium, you access your own claims data, and you avoid state insurance premium taxes (2–3% of premium in most states). The primary risk is claims volatility — a bad year can spike costs significantly above what a fully insured plan would have charged.

For a 150-person company with a relatively young, healthy workforce and at least 18 months of clean claims history, self-funding with stop-loss insurance (specific and aggregate) is worth modeling seriously. Level-funded plans — a hybrid product that provides monthly cost predictability with self-funded economics — have become the most common entry point for mid-market employers at 100–200 employees. Your broker should be presenting this option at every renewal.

How much should we budget for benefits cost inflation in 2026? +

Medical trend projections for 2026 are running 6–8% for most mid-market employers on fully insured plans. Specialty pharmacy — including GLP-1 drugs — is the most significant source of upward pressure, adding 1–2% to the baseline for plans with broad GLP-1 coverage. Employers with level-funded or self-funded structures may see different trend depending on their specific claims experience.

The practical budgeting guidance: assume 7% medical trend, model plan design adjustments that reduce that to 4–5%, and use the delta as your risk reserve. A broker who tells you they can hold your increase to 3% without showing you a specific plan design change is telling you what you want to hear, not what the data supports.

How do benefits costs in Houston compare to NYC and Miami? +

Geography is a meaningful variable in health insurance pricing. Houston — and Texas generally — runs 10–15% below national average for health insurance premiums, driven by a competitive carrier market and relatively lower provider reimbursement rates compared to the Northeast. Miami and South Florida are closer to national average, with some upward pressure from higher specialist utilization rates. NYC and the New York metro area run 15–20% above national average, driven by provider costs and regulatory requirements.

For a mid-market employer with offices in all three markets, this geographic variation needs to be reflected in the plan design and contribution strategy — a single plan that works at the Texas rate may be underfunded for New York. A broker with multi-market experience manages this; a single-market broker often doesn’t.

What is the most cost-effective benefits program for a 100-person company? +

Cost-effectiveness at 100 employees means getting competitive benefit quality at below-market cost — not simply the lowest possible premium. The most cost-effective structures typically combine a high-deductible health plan (HDHP) with employer HSA seed contributions, dental and vision at competitive employer-paid levels, basic life and disability as employer-paid with employee voluntary buy-up options, and a 401(k) match at the competitive floor for your industry.

The key is the benchmarking analysis that tells you what “competitive floor” means for your specific workforce and labor market. Spending above the market benchmark on benefits that employees don’t value is wasted money. Spending below the benchmark on benefits that drive retention decisions is an unquantified turnover cost. Your broker should be helping you find exactly that line — and adjusting it as your workforce and competitive environment change.

Disclaimer: Cost estimates in this article reflect mid-market benchmarking data as of 2025–2026 and are provided for planning context only. Actual costs depend on your specific plan design, workforce demographics, geography, and carrier relationships. Consult with our licensed benefits advisors for analysis specific to your organization.

Find Out Where Your Benefits Spend Stands

Hotaling Insurance Services runs independent cost benchmarking for mid-market employers managing $500K–$3M in annual benefits spend. We deliver industry-specific data matched to your company size and geography — and a concrete plan for your next renewal.

- ✓ $30.2M in managed employee benefits premium

- ✓ Multi-market expertise — Houston, Miami, NYC

- ✓ Self-funding and level-funding analysis for 100+ employee companies

- ✓ No carrier bias in our benchmarking

Serving Houston, Miami, and NYC. Minimum $1M annual premium.