Geopolitical Risk and Commercial Insurance: What the 2026 Energy Crisis Exposes in Your Coverage

Reading Time: 6 minutesGeopolitical Risk and Your Commercial Insurance: What the 2026 Energy Crisis Exposes in Your Coverage Key Takeaways for Risk Managers and CFOs The exposure is rarely the asset you own: most US companies hurt by a geopolitical shock have no property in the conflict zone. The loss comes through suppliers, contracts, and policy extensions that […]

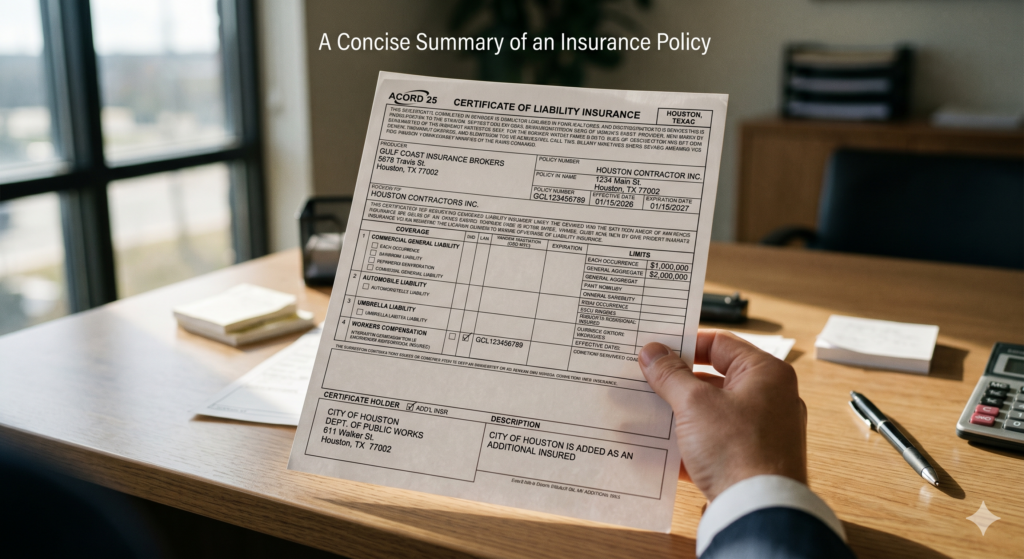

What Is a Certificate of Insurance (COI)? An Enterprise Guide to Vendor Compliance

Reading Time: 8 minutesWhat Is a Certificate of Insurance (COI)? A certificate of insurance (COI) is a one-page document that summarizes an active insurance policy: who is covered, what types of coverage are in force, the limits, and the dates the coverage runs. It is proof, not the policy itself, and that distinction is where most enterprise compliance […]

Single Tooth Implant Cost Without Insurance: 2026 Price Breakdown

Reading Time: 9 minutesSingle Tooth Implant Cost Without Insurance: 2026 Price Breakdown A single tooth implant runs between $3,000 and $6,000 out of pocket when you don’t have dental coverage. That range catches most people off guard — especially when the dentist quotes them a number that includes the surgical post, the abutment connector, and the porcelain crown […]

Nonprofit Insurance Requirements by State: What Your 501(c)(3) Legally Needs

Reading Time: 4 minutesNonprofit Insurance Requirements by State: What Your 501(c)(3) Legally Needs Nonprofit insurance requirements come from three sources that operate independently and sometimes inconsistently: state law, grantmaker requirements, and contractual obligations. Understanding which requirements are legally mandated versus contractually required — and in which states — prevents both compliance gaps and unnecessary over-coverage. Key Takeaways Workers’ […]

Workers Compensation for Nonprofits: Coverage for Staff, Contractors, and Volunteers

Reading Time: 6 minutesWorkers Compensation for Nonprofits: Coverage for Staff, Contractors, and Volunteers Workers’ compensation is legally required for nonprofit employees in virtually every state — and it’s one of the most misunderstood coverage lines in the nonprofit sector. The confusion typically involves three questions: which workers are actually covered, how premiums are calculated and controlled, and what […]

PEO Services for Nonprofits: Outsourcing HR When You Don’t Have an HR Department

Reading Time: 9 minutesPEO Services for Nonprofits: Outsourcing HR When You Don’t Have an HR Department A 40-person food bank doesn’t have a VP of Human Resources. What it has is an executive director who spends 15 hours a week on payroll questions, benefits enrollment issues, and trying to figure out whether the new hire in the satellite […]

Employee Benefits for Nonprofits: How to Compete for Talent on a Restricted Budget

Reading Time: 4 minutesEmployee Benefits for Nonprofits: How to Compete for Talent on a Restricted Budget The nonprofit talent market has changed. The assumption that mission-driven employees will accept below-market compensation indefinitely is no longer reliable — particularly in competitive urban markets where for-profit employers actively recruit from the same talent pools. Nonprofits that want to attract and […]

Key Person Life Insurance for Nonprofits: Protecting Against Executive Director Loss

Reading Time: 3 minutesKey Person Life Insurance for Nonprofits: Protecting Against Executive Director Loss Many nonprofits are operationally dependent on a single individual in a way that commercial businesses rarely are. The executive director who built the organization’s donor relationships over 20 years. The program director whose personal credibility drives government contract renewals. The development director whose major […]

How Much Does Nonprofit Insurance Cost? 2026 Benchmark Guide

Reading Time: 4 minutesHow Much Does Nonprofit Insurance Cost? 2026 Benchmark Guide Nonprofit insurance costs vary so widely — from under $5,000 annually for small community organizations to over $200,000 for large multi-site nonprofits with clinical programming — that general estimates are nearly useless without context. The cost is driven by five primary factors: organization budget and revenue, […]

Abuse and Molestation Liability Insurance for Nonprofits: What Organizations Working with Children Must Carry

Reading Time: 4 minutesAbuse and Molestation Liability Insurance for Nonprofits: What Organizations Working with Children Must Carry Abuse and molestation liability is the coverage most nonprofit leaders are aware of, most uncomfortable discussing, and most likely to have inadequate — or entirely missing — from their insurance program. The discomfort is understandable. The gap is not acceptable. Any […]