Builders Risk Insurance and Rising Construction Material Costs

Last month, a framing contractor working in The Heights called our office in panic. “Lumber prices jumped 30% since I bought my builders risk policy,” he explained. “I’ve got $200,000 in materials on-site. If they’re stolen tomorrow, will insurance cover today’s prices or what I paid?”

That question keeps contractors awake at night across Houston’s booming construction zones. Whether you’re protecting materials for a River Oaks custom estate, managing a downtown commercial project near Buffalo Bayou, or breaking ground in Katy’s expanding developments, builders risk insurance must evolve with volatile construction material costs. Here’s what Texas contractors need to know in 2025.

📊 Key Takeaways

- Builders risk insurance covers materials at replacement cost, but standard policies exclude market price increases

- Construction materials represent 40-50% of project costs, making adequate builders risk coverage critical

- Material price escalation endorsements protect against inflation beyond 5-10% thresholds

- Builders risk should start before first material delivery, not when construction begins

- Premium costs range from 1-4% of total construction value annually

Understanding Builders Risk Coverage for Construction Materials

Builders risk insurance acts as your project’s financial safety net, but many contractors misunderstand what it actually covers. Let me clear up the confusion we see daily.

What Builders Risk Insurance Actually Covers

Your builders risk policy protects construction materials against direct physical loss. This includes theft (the biggest claim we process), fire, vandalism, wind damage, and most weather events. Coverage extends to materials whether they’re on-site, in transit, or temporarily stored off-site within specified radius limits.

Here’s what surprises contractors: builders risk covers materials at replacement cost, not original purchase price. If copper pipe costs 20% more when stolen than when you bought it, standard policies pay current market rates. But there’s a catch – this only applies to covered losses, not general market increases.

The Gap: Why Standard Builders Risk Falls Short

Standard builders risk policies have a massive blind spot: material price escalation without a loss event. If steel prices double during your project, your coverage limits don’t automatically adjust. You’re underinsured without lifting a hammer.

One developer working on the East River mixed-use project learned this lesson painfully. His $5 million builders risk policy seemed adequate when materials cost $2 million. Six months later, those same materials cost $2.8 million. When storm damage struck during hurricane season, his coverage fell $800,000 short of replacement costs.

Houston’s Geographic Risks Amplify Coverage Needs

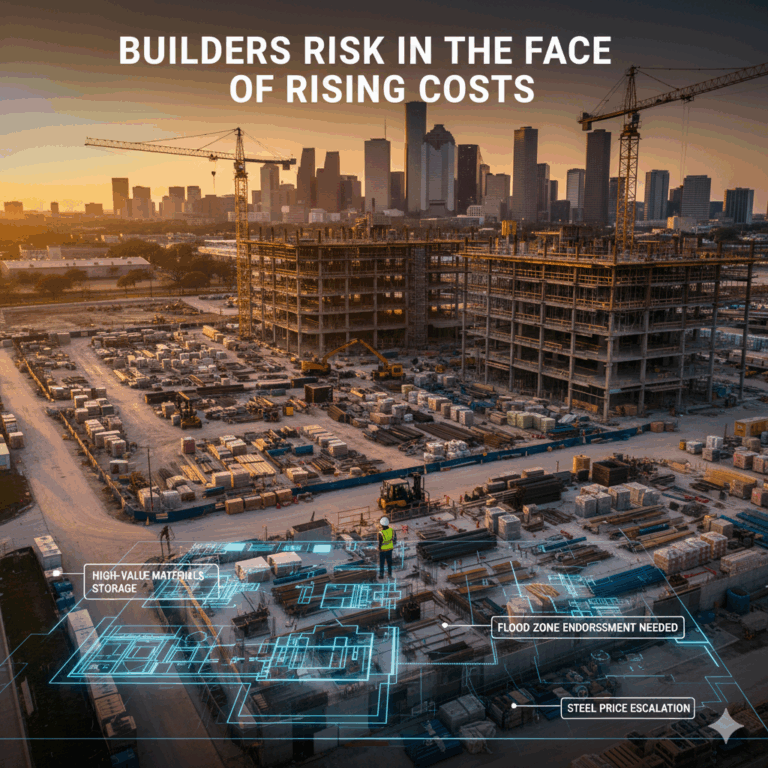

Houston’s unique geography creates additional builders risk challenges beyond material costs. Projects near our city’s extensive bayou system – particularly along Brays Bayou and White Oak Bayou – face elevated flood risks that standard builders risk policies often exclude. Materials stored at ground level in these flood-prone areas need specialized coverage endorsements.

Consider the western Inner Loop neighborhoods where land subsidence affects foundations. A Memorial Villages contractor discovered his stored concrete and rebar shifted due to ground movement, damaging $150,000 in materials. Standard builders risk wouldn’t cover this – he needed specific subsidence endorsements common in Houston but rare elsewhere.

How Construction Material Costs Impact Builders Risk Premiums

Your builders risk premium directly correlates with material values. Understanding this relationship helps you optimize coverage without overpaying.

| Project Type | Material % of Budget | Builders Risk Rate | Key Coverage Needs |

|---|---|---|---|

| Residential Frame | 40-45% | 0.3-0.5% | Lumber theft, weather protection |

| Commercial Steel | 45-50% | 0.25-0.4% | Material staging, crane coverage |

| Renovation | 35-40% | 0.4-0.7% | Existing structure, stored materials |

| High-End Residential | 50-55% | 0.5-0.8% | Specialty items, import coverage |

| Houston Flood Zone | 40-50% | 0.6-1.2% | Flood endorsement mandatory |

| Infrastructure | 35-45% | 0.2-0.35% | Equipment, aggregate materials |

Calculating Your Builders Risk Needs

Proper builders risk limits require accurate material cost calculations. Start with detailed quantity takeoffs, add current market prices, include 10% waste factors, and don’t forget delivery charges. The formula: Total Project Value = Materials + Labor + Overhead + Profit. Your builders risk limit should match this total, not just material costs.

Get Your Builders Risk Quote

Protect your materials from theft, damage, and price volatility. Our builders risk specialists design coverage for Texas contractors.

Critical Builders Risk Endorsements for Material Cost Protection

Smart contractors enhance standard builders risk with strategic endorsements. These additions transform basic coverage into comprehensive protection.

Inflation Guard Provisions

Inflation guard automatically increases your builders risk limits quarterly. For a 12-month project, we typically recommend 10-15% annual inflation protection. This endorsement costs roughly $200-400 extra but prevents devastating coverage gaps. Travelers and Chubb offer the most flexible inflation guard options we’ve seen.

Material Price Escalation Coverage

This game-changing endorsement covers cost differences when material prices spike beyond predetermined thresholds (usually 5-10%). If lumber jumps 25%, you’re covered for the excess. Few carriers offer true price escalation coverage – Cincinnati Insurance and Pure Insurance lead the pack here.

Soft Costs and Delay Coverage

When material shortages delay projects, costs mount quickly. Extended financing, additional rentals, lost income – these soft costs devastate budgets. Builders risk soft cost endorsements cover these expenses when covered losses cause delays. We’ve seen claims exceed $50,000 monthly on large projects.

Location-Specific Endorsements for Houston Projects

Houston’s top position for new-home construction brings unique risks requiring specialized builders risk endorsements. Projects in coastal areas like Kemah need storm surge protection beyond standard wind coverage. Downtown commercial developments near Buffalo Bayou require flood endorsements – flooding remains Houston’s primary natural hazard.

High-traffic corridors present different challenges. Construction along Westheimer Road or Upper Kirby faces elevated vandalism and theft risks. Materials for luxury builds in West University Place or Tanglewood attract professional thieves. These areas need enhanced security provisions and higher theft sublimits in builders risk policies.

🔍 Builders Risk Coverage Comparison

Basic Policy: Theft, fire, wind, vandalism at replacement cost

Enhanced Policy: All basic coverage PLUS inflation guard, soft costs, price escalation, equipment breakdown

Premium Difference: 20-30% higher

Potential Savings: 200-500% in uncovered losses

When Should Builders Risk Insurance Start?

Timing matters more than most contractors realize. Builders risk should begin when materials arrive on-site or construction starts – whichever comes first. We see too many claims denied because materials were delivered before coverage began.

A concrete contractor stored $75,000 in rebar on-site two weeks before his builders risk started. Thieves struck three days later. Claim denied. That expensive lesson taught him to coordinate coverage with delivery schedules, not construction starts.

Strategic Builders Risk Timeline

Bind builders risk coverage before first material delivery. Include off-site storage locations in your policy. Extend coverage through punch list completion. Consider completed operations coverage for post-construction issues. Never let coverage lapse during project delays – extensions cost pennies compared to potential losses.

Builders Risk Best Practices for Volatile Material Markets

Today’s construction environment demands adaptive builders risk strategies. Here’s what works:

Regular Coverage Reviews

Review builders risk limits quarterly on long projects. When material costs spike 10% or more, increase coverage immediately. Document material purchases with photos and invoices – claims adjusters need proof. Update your carrier about project scope changes that affect material quantities.

Security Measures That Reduce Premiums

Builders risk carriers offer significant discounts for security measures. Fenced job sites earn 5-10% discounts. Security cameras reduce premiums another 5-15%. GPS tracking on high-value materials impresses underwriters. Night lighting and guard services practically pay for themselves through premium savings.

Subcontractor Coordination

Require subcontractors to maintain their own builders risk for materials they supply. Verify coverage before materials arrive. Include waiver of subrogation clauses preventing their carriers from pursuing you after losses. Document material custody transfers – whoever controls materials needs coverage.

Builders Risk Coverage Analysis

Rising material costs demand comprehensive builders risk protection. Let’s review your current coverage and identify gaps before they become claims.

Real Claims: How Builders Risk Protects Material Investments

Theory meets reality when claims happen. These actual cases illustrate builders risk in action:

Case 1: Copper Theft – A Houston plumber stored $40,000 in copper for a medical building. Thieves struck overnight. His builders risk paid full replacement cost – $52,000 at current prices. Without replacement cost coverage, he’d have lost $12,000 to inflation.

Case 2: Storm Damage – Wind scattered a framer’s lumber across three acres. His builders risk covered collection, sorting, and replacement of damaged materials. Total claim: $85,000. His premium: $2,400. The math speaks for itself.

Case 3: Price Escalation Success – A developer with material price escalation coverage watched steel prices surge 35%. When fire destroyed his stockpile, enhanced builders risk covered the full replacement at new prices. Standard coverage would’ve left a $200,000 gap.

Navigating Builders Risk for Different Project Types

Residential Construction

Frame construction faces extreme lumber theft risk. Builders risk must include off-site coverage for materials stored at suppliers. Consider higher limits during framing phase when materials sit exposed. Add ordinance and law coverage for code upgrades required after losses.

Commercial Projects

Commercial builders risk needs equipment breakdown coverage for mechanical systems. Materials often require specialized handling – ensure your policy covers crane operations. Delay in completion coverage becomes critical with liquidated damage clauses. Require all trades to carry matching builders risk terms.

Renovation and Restoration

Existing structure coverage protects the building you’re improving. Builders risk should include discovered damage – problems found after work begins. Historic projects need specialized coverage for period-correct material replacements. Temporary protection measures during work require explicit coverage.

Related: vendor liability insurance

Frequently Asked Questions About Builders Risk and Material Costs

What does builders risk insurance cover for materials?

Builders risk insurance covers construction materials against direct physical loss including theft, vandalism, fire, wind, and weather damage. Coverage extends to materials on-site, in transit, and in temporary storage locations. Most builders risk policies cover materials at replacement cost, meaning you’ll receive current market prices for covered losses. However, standard builders risk doesn’t cover price increases without a loss event – you need specific endorsements for market inflation protection.

How much does builders risk insurance cost?

Builders risk insurance typically costs 1-4% of the total construction cost annually, or 0.3-0.5% for short-term projects. For a $1 million project, expect $3,000-$5,000 in premiums. Factors affecting your builders risk cost include project type, location, materials used, security measures, and coverage limits. Frame construction costs more than steel due to fire risk. Coastal projects pay higher rates for wind coverage.

Does builders risk cover material price increases?

Standard builders risk policies do NOT cover material price increases due to market fluctuations alone. Your builders risk pays replacement cost only after a covered loss like theft or damage. However, you can add inflation guard or material price escalation endorsements to your builders risk policy. These protect against cost increases exceeding 5-10% thresholds. Given today’s volatile material costs, these endorsements are essential.

What percentage of construction cost is materials?

Materials typically account for 40-50% of total construction costs, directly impacting your builders risk coverage needs. Higher material percentages require enhanced theft protection and price escalation coverage. Luxury projects may see 55% material costs, while simple structures might be 35%. Your builders risk limits should reflect total project value, not just material costs, to avoid coinsurance penalties.

When should builders risk insurance start?

Builders risk insurance should start when materials are delivered to the job site or when construction begins, whichever comes first. Many contractors mistakenly wait until work starts, leaving stored materials unprotected. Start your builders risk coverage before first material delivery. Include any off-site storage locations from day one. Coordinate policy dates with your material delivery schedule, not your construction timeline.

How to calculate material cost for construction?

Calculate construction material costs accurately to ensure proper builders risk coverage: Create detailed quantity takeoffs from blueprints, get current supplier quotes (never use outdated prices), add 5-10% waste factor, include delivery and storage costs, and apply regional price adjustments. Accurate calculations prevent underinsurance on your builders risk policy. Document all material purchases for potential claims.

See also: our guide on nonprofit D&O insurance.

Related: bonded company guide.

Disclaimer:

This article is for informational purposes only and does not constitute financial or insurance advice. Builders risk coverage needs vary significantly by project. Consult with qualified insurance professionals for specific guidance on your construction project and builders risk requirements.About the Hotaling Team

The Hotaling Insurance Services team brings three generations of experience protecting Texas builders with comprehensive builders risk coverage. As a nationally licensed, family-office insurance firm, we specialize in complex construction risks and builders risk policies that evolve with market conditions. Our consultative approach ensures your projects stay protected from groundbreaking to grand opening.

Last Reviewed: September 23, 2025