com/hotaling-insurance-blog/does-zenni-take-insurance”>whether Zenni accepts insurance for online eyewear purchases.

Painting Contractor General Liability Insurance: Cost and Coverage

Key Takeaways

- Limits are contract-set: institutional work often requires more than the standard $1M/$2M, plus a $5M+ excess tower.

- Completed-operations aggregate must scale to large annual job volume.

- Additional insured via CG 20 10 and CG 20 37, primary and non-contributory, with waiver of subrogation.

- Pollution is excluded from GL — a critical gap for spray and coatings work.

- Subcontractor controls directly affect your GL rating and audit at scale.

For a large commercial painter.

- Bodily injury and third-party property damage arising from painting operations.

- Products-completed operations — overspray, peeling, and finish failure surfacing after large jobs close.

- Defense costs, which on institutional disputes can rival the underlying claim.

- Additional-insured protection extended to GCs and owners as contracts demand.

- Personal and advertising injury tied to business operations.

Structure GL for the Contracts You Bid

For contractors with $1M+ premium programs, GL has to coordinate with excess, pollution, and surety. Our advisors structure it to match institutional contract requirements before a COI ever holds up your start date.com/commercial-insurance/houston-commercial-dump-truck-insurance”>dump truck insurance in Houston covers the bonding and MCS-90 requirements operators face on TxDOT projects. The financial mechanics of this coverage are explored further in our COI and vendor liability

Request a Coverage ReviewSmall single-crew operations are typically served well by State Farm, GEICO, or Progressive.

What GL Limits Do Commercial Painting Contracts Require?

Most painting contractors choose among a few standard limit configurations, and for large commercial work the contract usually dictates which one. The right structure depends on the size and type of projects you bid. Operators hauling on TxDOT contracts face distinct requirements, and our guide to dump truck insurance in Houston covers Harris County permitting and MCS-90 mandates.

- $1M per occurrence / $2M aggregate: the baseline most commercial clients require before allowing work to begin.

- $1M / $2M with a $2M products-completed-operations aggregate: standard where post-completion finish defects are the concern.

- Primary limits plus a $5M–$25M excess tower: required on institutional, public, and high-rise contracts.

- The completed-operations aggregate should match annual job volume, since painting defects surface months after a job closes.

- Higher limits are satisfied through a commercial umbrella sitting above the primary GL.

How Additional-Insured Endorsements Decide Whether You Win the Job

Tenants often underestimate what they stand to lose — our guide to the benefits of renters insurance covers what the policy protects. For more details, see our guide on renters insurance coverage details.

Liability extends beyond business operations — our guide to personal liability insurance explains individual coverage options. Learn more about excess personal liability coverage. The financial mechanics of this coverage are explored further in our umbrella insurance analysis guide.

Specialty trade contractors face similar coverage requirements across disciplines — for details on how licensing and liability intersect for mechanical trades, see our guide to HVAC contractor insurance costs.

Painting contractors working on construction projects need to understand how their coverage fits within the broader insurance requirements — see our guide to construction insurance requirements for contractors for the full landscape.

Painting contractors on construction projects should confirm builders risk coverage protects their installed work — see our breakdown of builders risk insurance pricing for how premiums are calculated.

- CG 20 10 extends additional-insured status for ongoing operations; CG 20 37 covers completed operations.

- The edition date governs scope: a 10/01 edition responds regardless of fault, while a 07/04 edition can require fault first.

- Contracts typically require primary and non-contributory wording so your policy responds before the GC’s.

- A waiver of subrogation is commonly required, preventing your insurer from pursuing the GC after a loss.

- A COI that does not match the contract’s exact endorsement language holds up your start or costs you the award.

What GL Does Not Cover: The Pollution and Workmanship Gaps

Two exclusions catch large painters by surprise, and both require deliberate coverage decisions rather than assumptions about what the GL policy includes.

- Pollution exclusion: standard GL excludes pollution, so spray, VOC, solvent, and abrasive-blasting exposures require a separate contractors pollution liability policy.

- The “your work” exclusion: GL generally does not pay to redo your own defective workmanship, only the resulting third-party damage.

- Surface-prep, paint-failure, and color-matching disputes are often addressed through a GL endorsement with sublimits or a contractor’s E&O policy.

- This workmanship endorsement is critical for specialty finishes, exterior work, and engineered coating systems.

- Coordinating these gaps with the GL placement is where a specialist broker prevents an uncovered loss.

What Drives GL Premium for a Large Painting Operation?

How Much Does Painting Contractor GL Insurance Cost?

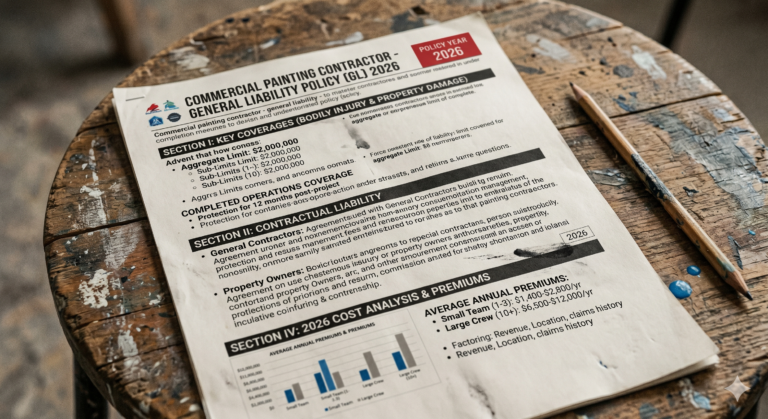

General liability premiums for commercial painting contractors range from $2,500 to $12,000 per year, depending on annual revenue, payroll size, number of employees, and whether the work is residential, commercial, or industrial. Contractors doing interior residential work sit at the low end. Contractors handling exterior commercial work at height, industrial coatings, or lead-paint abatement push toward the high end because the exposure profile is fundamentally different.

| Operation Type | Annual Revenue | Employees | Annual GL Premium |

|---|---|---|---|

| Residential interior only | $500K–$1M | 5–10 | $2,500–$4,500 |

| Residential interior + exterior | $1M–$3M | 10–25 | $4,000–$7,500 |

| Commercial / multi-family | $3M–$8M | 25–60 | $6,000–$10,000 |

| Industrial / lead abatement | $5M+ | 40+ | $8,000–$12,000+ |

The rating basis for painting contractor GL is typically per $1,000 of revenue or per $1,000 of payroll, depending on the carrier. Most painting contractors are rated under NCCI class code 91560 (painting operations) or a state-equivalent code. The base rate runs $3.50–$8.50 per $1,000 of revenue nationally, with credits or surcharges based on claims history, years in business, and safety program documentation. Contractors with a formal safety program and no claims in the past three years typically qualify for 10–25% schedule credits that meaningfully reduce the premium.

Frequently Asked Questions

What GL limits do large painting contracts require? +

Standard minimums are $1M per occurrence / $2M aggregate, but institutional, public, and high-rise contracts frequently require higher primary limits plus a $5M–$25M excess tower. The completed-operations aggregate should be sized to your annual job volume.

Does painting GL cover pollution from coatings? +

No. Standard GL excludes pollution. Spray, VOC, solvent, and abrasive-blasting exposures require a separate contractors pollution liability policy — essential for industrial and infrastructure coatings work.

Does GL cover defective workmanship like paint failure? +

Generally not directly. GL’s “your work” exclusion means it does not pay to redo your own defective work, only resulting third-party damage. Surface-prep and coating-failure disputes are addressed through a GL endorsement with sublimits or a contractor’s E&O policy.

How does subcontracting affect GL cost? +

Using uninsured or underinsured subcontractors transfers their exposure to your policy and rolls their cost into your audit as covered payroll, raising premium. For additional guidance, explore our resource on professional employer organization insurance. Enforcing downstream insurance requirements and collecting current COIs is a primary cost-control lever at scale.

What is the right completed-operations aggregate? +

It should match your annual job volume. Painting defects like peeling and overspray surface months after completion, so a large operation needs a completed-operations aggregate sized to the work it actually puts out, not a default minimum.

About the cost figures and examples in this article: Any premium ranges, cost figures, or pricing factors discussed here are general market estimates drawn from publicly available industry data and are provided for educational context only. They are not quotes, offers, or guarantees of cost, and they do not reflect the price Hotaling Insurance Services will or can offer for any specific policy. Actual premiums are determined solely by the insurance carrier based on your individual risk profile, coverage selections, claims history, location, and other underwriting factors, and they vary widely from the general ranges described above. Any client scenarios are anonymized, illustrative composites created for educational purposes; they do not depict actual named clients and should not be relied upon as a prediction of results. Nothing in this article constitutes financial, legal, tax, or insurance advice. For pricing and coverage specific to your organization, please request a consultation with our licensed advisors.